Find the best Trust Accounting Software

Compare Products

Showing 1 - 20 of 50 products

Sort by

Reviews: Sorts listings by the number of user reviews we have published, greatest to least.

Sponsored: Sorts listings by software vendors running active bidding campaigns, from the highest to lowest bid. Vendors who have paid for placement have a ‘Visit Website’ button, whereas unpaid vendors have a ‘Learn More’ button.

Avg Rating: Sorts listings by overall star rating based on user reviews, highest to lowest.

A to Z: Sorts listings by product name from A to Z.

Clio

Clio

Ranked #1, Clio is the leading law practice management software used by over 150,000 lawyers and with the most 5-star reviews. The only legal software with 1,500+ reviews on Capterra. Lawyers can access and manage their work in ...Read more about Clio

MyCase

MyCase

MyCase is a cloud-based legal management solution that helps attorneys in small to medium size law firms manage communications with their clients and carry out daily business operations. The solution also provides functionalities ...Read more about MyCase

Smokeball

Smokeball

Smokeball is the only cloud-based legal case management software that also runs from your desktop. Manage all of your matters with collaborative case management; customize your commonly used forms with a single click in document a...Read more about Smokeball

CARET Legal

CARET Legal

CARET Legal is the leading solution for legal professionals to manage their practice and create space for what matters, including delighting clients and maximizing billable time. From client intake, to matter management, to bac...Read more about CARET Legal

Talk with us for a free

15-minute consultationSoftware Advice is free because vendors pay us when they receive sales opportunities.

This allows us to provide comprehensive software lists and an advisor service at no cost to you.

This allows us to provide comprehensive software lists and an advisor service at no cost to you.

Meet Eric, a software expert who has helped 1,534 companies select the right product for their needs.

Talk with us for a free

15-minute consultationSoftware Advice is free because vendors pay us when they receive sales opportunities.

This allows us to provide comprehensive software lists and an advisor service at no cost to you.

This allows us to provide comprehensive software lists and an advisor service at no cost to you.

Tell us more about your business and an advisor will reach out with a list of software recommendations customized for your specific needs.

STEP 1 OF 4

How many users do you have?

Curo365

Curo365

Built on the most powerful cloud-based solution, Curo365 resides on the Microsoft Dynamics 365 platform built specifically for law firms and integrates with your existing Microsoft Office 365 applications. The only singular soluti...Read more about Curo365

QuickBooks Online

QuickBooks Online

QuickBooks Online is a small business accounting software and app that allows you to manage your business anywhere, anytime. Used by over 7 million customers globally, QuickBooks provides smart tools for your business, yet is easy...Read more about QuickBooks Online

Xero

Xero

Xero is a global small business platform with 3.95 million subscribers which includes core accounting, payroll, workforce management, expenses and projects. Xero also has an extensive ecosystem of connected apps and connections to...Read more about Xero

BQE CORE Suite

BQE CORE Suite

BQE’s powerful all-in-one platform and expert support give Architecture, Consulting, and Engineering firms the intuitive tools they need to meet the demands of their firm, empower their team, maximize profitability, and deliver su...Read more about BQE CORE Suite

TimeSolv Legal Billing

TimeSolv Legal Billing

TimeSolv is a cloud-based legal time tracking and billing solution that caters to law firms, accountants, consultants, architects, and freelancers, helping them manage daily business operations. TimeSolv integrates project ma...Read more about TimeSolv Legal Billing

Zoho Books

Zoho Books

Zoho Books comes with automatic bank feeds, collaborative client portal, accounting and taxing, online payments, invoice templates and analytical reports. The system allows users to manage multiple time sheets of different project...Read more about Zoho Books

PracticePanther Legal Software

PracticePanther Legal Software

PracticePanther Legal Software is a legal management solution for small to large practices specializing in areas including bankruptcy, personal injury, family, divorce, estate planning, litigation, criminal law and many more. The ...Read more about PracticePanther Legal Software

Sage Intacct

Sage Intacct

Sage Intacct is a provider of cloud-based financial management and accounting software. Sage Intacct's software solution is suitable for small to midsize accounting firms and can provide financial reporting and operational insight...Read more about Sage Intacct

AbacusLaw

AbacusLaw

AbacusLaw is case automation software designed explicitly for law firms. The system works as a complete practice management solution that helps in managing workflows including time tracking, billing, and accounting operations. Aba...Read more about AbacusLaw

CosmoLex

CosmoLex

CosmoLex is a cloud-based legal management solution that offers features including time tracking, billing, trust accounting, task and document management. The solution connects all modules so that users do not have to enter i...Read more about CosmoLex

LEAP

LEAP

LEAP is the legal practice productivity solution designed to help small to mid-sized law firms improve efficiency, productivity, and profitability. LEAP leverages best-in-class technology to help law firms with practice management...Read more about LEAP

Rocket Matter

Rocket Matter

Rocket Matter is a cloud-based legal billing and management solution designed to cater small and midsize law practices. It features time and billing management, calendar, document management, payments and collaboration management ...Read more about Rocket Matter

Bill4Time

Bill4Time

Bill4Time is a cloud-based professional services system that offers time and expense tracking, billing and invoicing, and project management capabilities to many different industries. The system records billable and non-billable...Read more about Bill4Time

Tabs3

Tabs3

Tabs3 Software offers practice management, case management and financials for small to midsize firms in any practice area. Choose from Tabs3 Cloud, hosted, and on-premises server options; all include outstanding US-based support. ...Read more about Tabs3

Actionstep

Actionstep

With Actionstep, midsize law firms get total control over their future success. Actionstep's comprehensive legal business management platform is built to adapt to a firm’s unique strengths and goals, empowering firms to modernize ...Read more about Actionstep

MYOB Business

MYOB Business

MYOB Business accounting software is designed to help businesses of any size across Australia and New Zealand take care of GST, invoices, reporting, expenses & payroll (including Single Touch Payroll). Designed to save time, incre...Read more about MYOB Business

Popular Comparisons

Buyers Guide

Last Updated: March 16, 2023Trust accounting is a complex, niche field that spans the financial and legal industries. Dedicated software can make trust accounting easier to handle, but successful implementation requires an understanding of specifically how that software can help lawyers, accountants and other parties manage trust funds and the assets that those funds produce.

This buyer’s guide will not only serve as a primer on what trust accounting is, but also explain what specific things software buyers should look out for if they’re in the market for a trust accounting system.

Here’s what we’ll cover:

What Is Trust Accounting Software?

What Is Legal Trust Accounting?

Common Features of Trust Accounting Software

What Is Trust Accounting?

In its largest sense, the term "trust accounting" refers to the financial management of trust accounts—accounts in which a trustee holds funds for some specific purpose.

When talking about general trust accounting, though, we are more specifically referring to accounts created as a part of estate planning (the dispersal and management of a person's assets after their death).

Adding to the confusion is the fact that this form of trust accounting, or "fiduciary accounting," has a counterpoint in the legal profession. Although legal firms are frequently involved in trust accounting for estate planning and other purposes, "legal trust accounting" refers to a different, separate practice.

What Is Legal Trust Accounting?

Lawyers create legal trust accounts for a few reasons, including:

They have been given advance fees (such as retainers) by clients

They are holding funds for clients in connection with payment of a settlement

They are holding client funds as a fiduciary for that client

By law, these accounts must be separate from the lawyer's own personal or business account, making legal trust accounting an essential part of legal practice and ethics.

In many cases, these trusts are eligible for the IOLTA (Interest on Lawyers Trust Accounts) program, which takes the interest from lawyers' trust accounts and uses it to provide legal aid on civil matters to low-income families and individuals. All 50 states currently have an IOLTA program.

According to the program's website, "A lawyer who receives funds that belong to a client must place those funds in a trust account separate from the lawyer's own money. Client funds are deposited in an IOLTA account when the funds cannot otherwise earn enough income for the client to be more than the cost of securing that income. The client—and not the IOLTA program—receives the interest if the funds are large enough or will be held for a long enough period of time to generate net interest that is sufficient to allocate directly to the client."

One of the main features of legal trust accounting software is automated management and accounting of those IOLTA funds, making lawyers the primary customers of trust accounting software vendors.

The products we'll be discussing in this guide are specifically geared toward legal trust accounting, though we will be referring to it as "trust accounting" for simplicity's sake.

Common Features of Trust Accounting Software

Different trust accounting systems will have different features, depending in part on how integrated they are with a more robust suite of legal and/or accounting software. The most typical features are explained in the following chart.

Create financial statements tracking funds across multiple trust accounts. Lawyers must be able to produce a report showing how funds in a trust account are used. This also allows you to reconcile trust accounts every month and be audit-ready should the need arise. | |

Almost all trust accounting software integrates with (or comes in a suite with) more generalized legal billing/timekeeping software that allows for easy creation of invoices and payment collection, while squaring those exchanges with trust accounts. | |

Some trust accounting software integrates with general legal accounting software, so all financial records are housed in the same database and trust accounts match up with overall financials. | |

Track the ledgers of multiple accounts for multiple clients, avoiding the mistake of commingling accounts. Organize by legal matter or client to customize according to your preference. | |

IOLTA accounting | For accounts that qualify, track the interest accrued, make automatic payments into the program and make sure you are abiding by the IOLTA rules of your state. |

Trust account automation | Some systems will apply trust monies directly through automatic billing, keeping the accounts balanced without the need for manual transactions. |

Compliance | Many states have laws that regulate how attorneys can maintain lawyers' trust accounts. Software can help you make sure you follow all relevant local and national legislation. |

Accountant/bookkeeper access | Some trust accounting systems provide free account access for an external financial advisor, so that you can have your chosen expert double-check your compliance. |

What Type of Buyer Are You?

Although lawyers and law firms are the primary buyers of this type of software, they are not the only parties interested in legal trust accounting. Other buyers might include: bank trust departments, independent trust companies, accountants/CPAs, family offices, guardians, foundations and nonprofit organizations.

However, most buyers will be lawyers and law firms, falling into one of the following three categories:

Solo law practice. These are practices with only one attorney, who may or may not also have an outside bookkeeper. More frequently, however, these attorneys will keep their own records, and thus, trust accounting software will be crucial to monitor any trust accounts and abide by all state and federal regulations. These buyers will most likely have a need for other legal software functions, with trust accounting as part of a larger system.

Small or midsize law firm. These are practices with multiple lawyers, and most likely have an on-staff or outsourced accountant. Legal billing software will be of crucial importance for that accountant (or to the individual attorneys if there is no bookkeeper), and trust accounting software should be considered a vital component of that software suite.

Large law firm. These are firms with many partners and associates, and a full accounting team. They will require a robust software system that includes billing, case management and legal document management. Trust accounting software, as one component of that system, will be extremely important, to make sure that the multiple trust accounts of various attorneys in the firm are maintained ethically, legally and accurately.

Benefits and Potential Issues of Trust Accounting Software

A trust accounting software system allows for easier, more automated management of attorneys' trust accounts. Though just a small part of running a law practice, trust accounts are nevertheless extremely important, and need to be properly handled. Trust accounting software can make this easier. Some benefits of using this software include:

Ethical and legal compliance. Trust accounting software can help you make sure you follow all the rules of ethics and law surrounding trust accounts in your state. This will increase your accountability to your clients, to yourself and to the state bar.

Separation of accounts. Software will let you keep track of multiple accounts so you don't run the risk of accidentally commingling client funds with your own accounts.

Increase client/audit readiness. If your client asks for reports about their account, or if you should be audited, trust accounting software ensures that you have proper, thorough records of all transactions, including deposits, payments, interest etc.

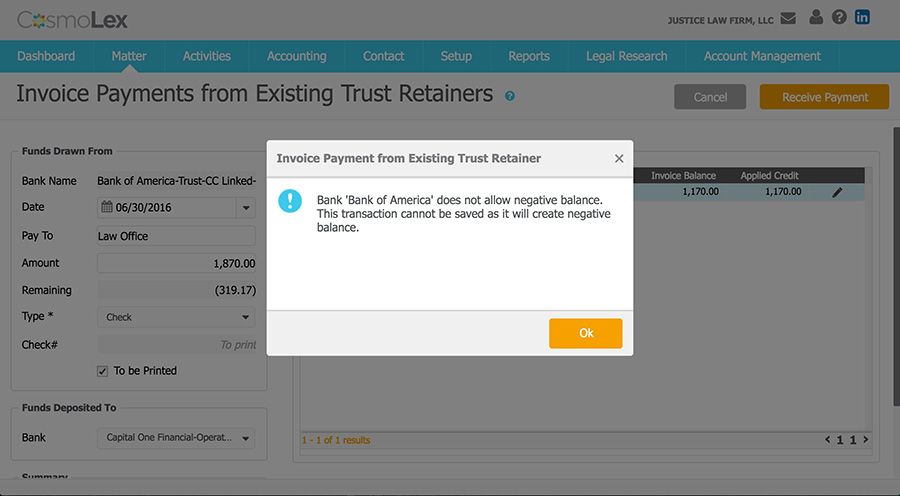

An example of CosmoLex trust accounting preventing an error

However, an overreliance on software is always a danger. In the case of the legal profession, making a mistake with your software will not save you from potential ethics violations or legal repercussions. Be sure you aren't just blindly following the software, and that you are well-informed about local and federal regulations regarding legal trust accounting. The software will aid you in managing those trusts, but it does not replace your own required due diligence.

Market Trends to Understand

Here are some market trends you should consider as you select a product:

Cloud-Based Software. Cloud-based systems are increasingly popular. They require less hardware than on-premises software as well as less IT knowledge, have lower upfront costs, and are more quickly implemented, making them a good choice for smaller firms/businesses, in particular.

Mobile functionality. As with most software at the moment, trust accounting systems are beginning to add mobile functionality, allowing you to access your software from a phone or tablet. This is particularly beneficial to solo firms where you can't be constantly bound to the office.